One of the BIGGEST MISTAKES one can make is the failure to screen an applicant before taking a security deposit and signing a lease.

You must be aware of the Fair Credit Act – and understand both Federal and State Law when accepting and deciding who gets to rent your unit. In other words – you may not discriminate. Certain exclusions apply. *** Please note the law(s) are very clear, this is only a brief note to warn you.

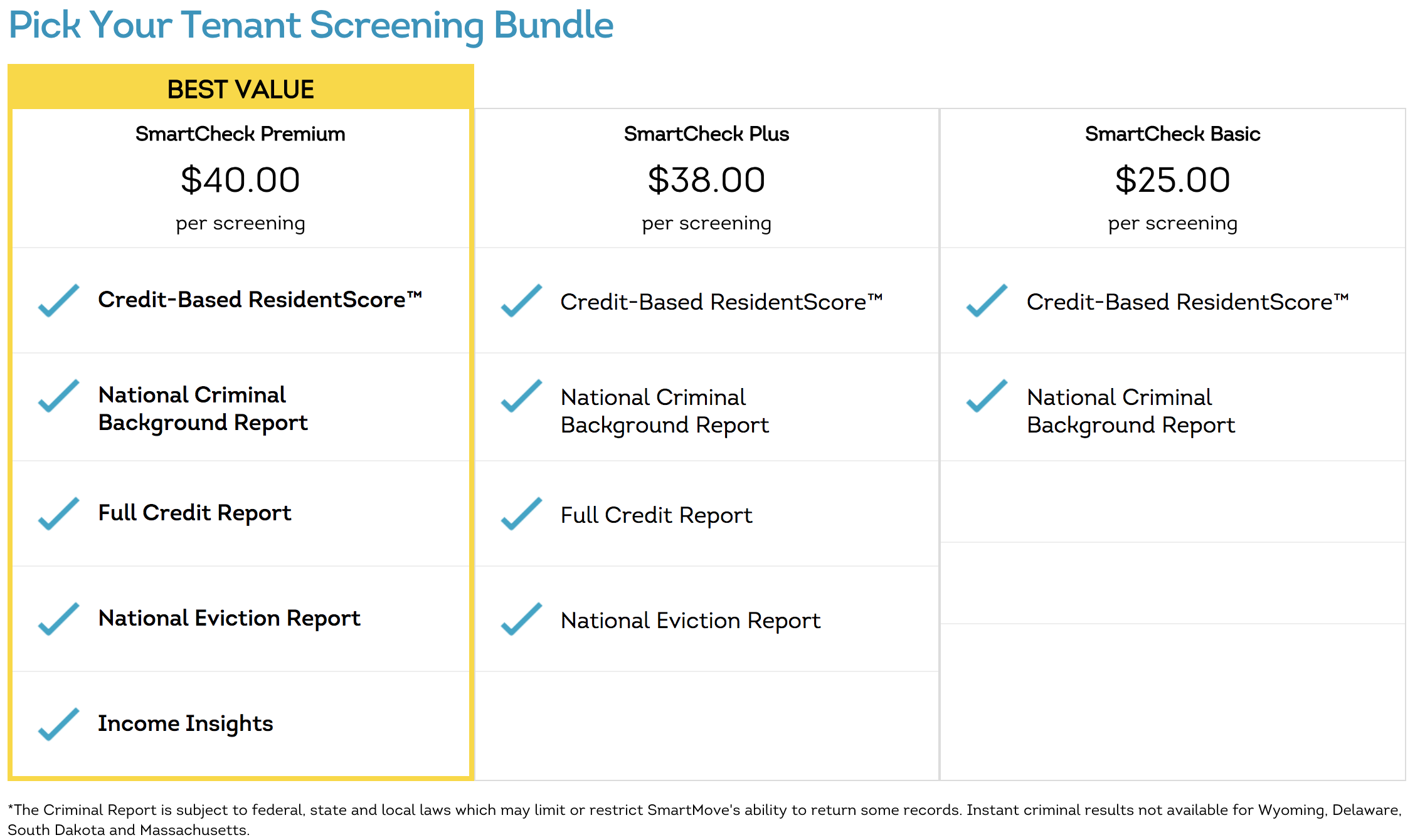

TENANT SCREENING FROM RENTLAW.com – START NOW

1. HAVE THE APPLICANT COMPLETE A RENTAL APPLICATION ( USE OUR FREE RENTAL APPLICATION HERE )

2. Get references and verify them

3. Login or Signup to our Tenant Screening Service. FREE for Landlords Here.

4. Based on the results of the credit report and verified references, decide whom to rent to.

5. Collect the first month rent and security deposit as permitted by law.

6. SIGN THE LEASE with the Tenant(s) – all of them over legal age. Be sure to copy the Driver License and Social Security Card if available. You want to have positive ID in case of eviction. **** Plenty of on-line sites tell you or scare you NOT to collect this information. BS – collect it and store it securely. Destroy it when legally permitted or when tenant leaves.

6. Give the tenant(s) a receipt for EVERYTHING and a COPY OF THE LEASE.

6a.USE OUR FREE LEASE HERE (Review it for your state – this is a sample).

6b.Add to this whatever decision criteria you have. You may want to check with a lawyer in your state to make sure it is enforceable (legally valid).

These steps may not guarantee the tenant will pay, but if you have to proceed to evict a tenant or they are late and you have to collect back rent, the more information you have, the easier it will be trace them down and MAYBE collect the rent due.